Buying a New Home PLR Course 27k Words

in PLR Checklists , PLR eBooks , PLR eCourses , PLR List Building Reports , Premium PLR , Premium PLR eBooks , Premium PLR Reports , Premium White Label Brandable PLR Coaching Courses , Private Label Rights Products , Real Estate , Real Estate PLR , Real Estate PLR eBooksChoose Your Desired Option(s)

has been added to your cart!

have been added to your cart!

#buyingahome #newhomeguide #realestateplr #homebuyingtips #plrcourse #propertyinvestment #homeownership #realestatecontent #firsttimebuyer

Buy Quality PLR presents: Buying a New Home PLR Course

Everything You Need to Know About Purchasing Your Dream Home – Fully Customizable PLR Course

Are you looking for a way to offer comprehensive, actionable, and high-value content to your audience while saving time and resources? The “Buying a New Home” PLR Course is your perfect solution. This extensive course, totaling 24,850 words, provides a step-by-step guide that walks your audience through the entire process of buying a new home, from defining their priorities to settling in and making the new house a home.

Whether you’re a real estate agent, coach, consultant, or content creator, this PLR course is designed to make the home-buying process easier for your audience while helping you grow your business by offering high-quality, informative content.

Presenting…

Buying a New Home PLR Course 27k Words

What’s Included in the Buying a New Home PLR Course?

Course Overview

- Course Title: Buying a New Home

- Word Count: 24,850 words

- Modules: 5 Comprehensive Modules

- Supplementary Materials:

- Buying a New Home – Checklist (667 words)

- Buying a New Home – FAQs (1,077 words)

- Buying a New Home – Salespage (850 words)

Course Structure and What You’ll Get in Each Module

This course is designed to take potential homebuyers through the entire process, from the first stages of research to finally moving in. Each module focuses on a specific stage of the process, offering valuable guidance and expert tips that will give your audience confidence in their ability to make informed decisions.

Module 1: Understanding Your Needs and Budget

In this first module, you’ll help your audience set a solid foundation for their home-buying journey. By understanding what they need versus what they want, they will be better prepared to make financially sound decisions.

- Step 1: Define Your Priorities

This step emphasizes the importance of creating a list of must-haves (e.g., number of bedrooms, location, amenities) versus nice-to-haves, so buyers can focus on what’s most important to them. - Step 2: Determine Your Budget

An essential part of the process, this section helps buyers calculate their maximum budget, including savings, potential loans, and other financial resources. The clearer they are on their budget, the easier it will be to make choices that are financially feasible. - Step 3: Research Financing Options

A thorough understanding of financing options is key to making an informed decision. This part of the course helps buyers navigate different types of mortgages (fixed-rate, variable-rate, government-backed loans) and decide which one fits their financial situation best. - Step 4: Set Realistic Expectations

With a clear understanding of their budget and financing options, buyers can then set realistic expectations for what they can afford in their desired market.

Module 2: Searching for Your Ideal Home

This module dives into the practical side of searching for the perfect property. Armed with realistic expectations, your audience will learn how to find the right home that aligns with their needs and budget.

- Step 1: Choose the Right Neighborhood

Location is one of the most important factors when buying a home. This section helps your audience identify neighborhoods that align with their lifestyle, considering factors like schools, commute times, safety, and local amenities. - Step 2: Start Your Home Search

This section introduces useful tools such as online listings, apps, and real estate agents to help buyers kickstart their home search. By exploring these options, they can identify potential properties that meet their needs. - Step 3: Attend Open Houses and Viewings

It’s essential to view multiple properties before making a final decision. This section provides tips for maximizing the effectiveness of open houses and viewings by taking notes, asking the right questions, and assessing each property based on what matters most. - Step 4: Keep Notes and Take Photos

To help buyers make an informed decision, this step encourages them to document each property they visit. Keeping detailed notes and photos of each home will make it easier to compare and evaluate different properties.

Module 3: Making the Offer and Negotiating

Once your audience has narrowed down their options, this module provides guidance on making a competitive offer and negotiating the best deal.

- Step 1: Understand Market Trends

Researching recent sales in the area is vital for understanding what’s reasonable to offer. This step teaches your audience how to research and evaluate market trends and home values to ensure they’re not overpaying. - Step 2: Work with a Real Estate Agent

A skilled real estate agent is a valuable ally during negotiations. This section highlights the importance of partnering with an agent who understands the local market and can help buyers negotiate a fair price. - Step 3: Negotiate Effectively

Negotiation can make or break a home purchase. This part of the course shares strategies for negotiating on price, repairs, or closing costs, ensuring buyers get the best possible deal. - Step 4: Get the Offer in Writing

Once terms have been agreed upon, it’s essential to get everything in writing. This step ensures buyers understand the legalities of their offer and avoids misunderstandings in the future.

Module 4: Closing the Deal

The final steps before homeownership involve thorough due diligence and the completion of paperwork. This module prepares your audience for the closing process.

- Step 1: Arrange a Home Inspection

A professional home inspection helps buyers identify any hidden problems with the property. This section explains the importance of hiring an inspector to assess the home’s condition. - Step 2: Finalize Financing

Buyers will need to finalize their mortgage application and ensure that everything is in place for the loan approval. This step guides them through the necessary steps to secure their financing. - Step 3: Review All Documents

Carefully reading all documents before signing is critical to avoiding future issues. This step walks buyers through the important documents they’ll encounter and helps them understand what they’re agreeing to. - Step 4: Schedule the Closing Date

Once everything is in place, buyers need to schedule the closing. This part of the course covers the final logistics of coordinating with the seller, agent, and lender to finalize the deal.

Module 5: Moving In and Settling Down

The final module offers practical advice for managing the move and ensuring everything is in order after the purchase.

- Step 1: Plan Your Move

Moving can be stressful, but careful planning can make it easier. This step includes creating a moving checklist and scheduling movers to help ease the burden. - Step 2: Update Your Address

This step helps buyers remember to notify banks, utility companies, and other important contacts of their new address. - Step 3: Set Up Utilities and Services

Arranging for utilities like electricity, water, and internet before moving in ensures the home is ready to live in on day one. - Step 4: Make Your New House a Home

Finally, after all the hard work, it’s time to unpack, decorate, and settle into the new space. This step includes advice on how to personalize the home and make it feel comfortable and welcoming.

What’s Included in the “Buying a New Home” PLR Course Package?

- Course Content (24,850 words) – 5 expertly crafted modules, covering all aspects of the home-buying process.

- Buying a New Home – Checklist (667 words) – A helpful checklist summarizing the key steps in the home-buying process.

- Buying a New Home – FAQs (1,077 words) – Common questions and answers to help buyers navigate their concerns.

- Buying a New Home – Sales Page (850 words) – A ready-to-use sales page that can help you market the course and attract customers.

How You Can Use and Profit from the “Buying a New Home” PLR Course

- Sell the Course: Package the course into an online course or digital download and sell it on your website or through platforms like Udemy, Teachable, or Skillshare.

- Lead Magnets: Break the course into smaller sections or modules and offer them as free content in exchange for email sign-ups, which you can later use for additional marketing.

- Online Coaching: Use the course as the foundation for an online coaching program, helping buyers through the process with personalized guidance.

- Affiliate Marketing: Include affiliate links in the course content, offering recommended tools, services, and products related to home-buying, such as mortgage lenders or home improvement companies.

- Membership Sites: Offer access to the course as part of a subscription-based membership site where members can access ongoing content on real estate and homeownership.

Take Action Now and Offer Your Audience Expert-Level Guidance on Buying a New Home!

By purchasing the “Buying a New Home” PLR Course, you can quickly provide high-quality, valuable content to your audience. Whether you want to create an online course, attract more leads, or build a membership site, this course is the perfect resource to boost your business.

Don’t wait any longer—start helping your audience navigate the exciting and important journey of buying a home today!

has been added to your cart!

have been added to your cart!

Here A Sample of Buying a New Home PLR Course

Welcome to the course “Buying a New Home”! This step-by-step guide is designed to walk you through the exciting journey of purchasing your dream home. By the end of this course, you’ll feel confident and informed about the entire process. Let’s dive in!

Module 1: Understanding Your Needs and Budget

Step 1: Define Your Priorities

Defining your priorities is a foundational step in the home-buying process. It helps you focus your search and avoid distractions while ensuring your final choice aligns with your needs and lifestyle. Here’s a detailed breakdown to guide you through this process step-by-step:

1. Reflect on Your Lifestyle Needs

Before making a list, take time to assess how you live today and how you envision your life in the new home. Consider factors like family size, work arrangements, and hobbies. Ask yourself:

- Who will live in this home? Account for partners, children, elderly parents, or pets.

- What are your daily habits? For example, do you work from home or need a home gym?

- What activities do you enjoy? Do you need outdoor space for gardening, a large kitchen for entertaining, or proximity to parks for recreation?

Use these reflections to identify your top priorities.

2. Categorize Must-Haves and Nice-to-Haves

This step ensures you have a clear understanding of what you absolutely require versus features you’d love but can live without.

- Create Two Columns: Draw two columns on a sheet of paper or use a digital tool like a spreadsheet. Label one column “Must-Haves” and the other “Nice-to-Haves.”

- Define Your Must-Haves: Must-haves are non-negotiable features essential for your comfort or practicality. Examples include:

- Number of bedrooms and bathrooms: Decide based on the current household size and future needs.

- Location: Consider proximity to work, schools, public transport, or specific neighborhoods.

- Safety and security: Research crime rates or check for gated communities.

- Accessibility: If you or family members have mobility concerns, prioritize features like ramps or elevators.

- List Nice-to-Haves: Nice-to-haves are desirable features that enhance your living experience but are not essential. Examples include:

- A large backyard.

- Open-concept design.

- A swimming pool, fireplace, or modern kitchen upgrades.

3. Prioritize Your Needs

After creating your lists, rank each item by importance within its respective category.

- For Must-Haves: Order the list by necessity. For example:

- Proximity to schools.

- At least 3 bedrooms.

- Safe neighborhood.

- For Nice-to-Haves: Order by desirability. For example:

- Energy-efficient appliances.

- Spacious outdoor area.

- Home office space.

4. Balance Current and Future Needs

Think beyond your immediate requirements and factor in long-term goals to ensure your new home supports your evolving lifestyle:

- Family growth: Will you need more rooms if you plan to have children or accommodate guests?

- Work flexibility: Do you need a dedicated home office as remote work becomes more common?

- Aging in place: Consider features like single-story layouts or low-maintenance designs.

5. Engage All Stakeholders

If you’re purchasing the home with a partner, family members, or others, it’s essential to get everyone’s input:

- Host a discussion to ensure the lists reflect everyone’s priorities.

- Agree on key must-haves to avoid conflicts during the search.

- Use tools like collaborative spreadsheets or checklists to combine and rank preferences.

6. Document Your Lists

Create a clean and organized record of your priorities. This might be:

- A physical checklist to carry during home viewings.

- A digital list in a shared app like Google Sheets for easy updates.

- A visual chart or infographic that categorizes features clearly.

For example, a table might look like this:

| Feature | Must-Have | Nice-to-Have |

| 3 Bedrooms | ✓ | |

| Open Concept Design | ✓ | |

| Proximity to Work | ✓ | |

| Large Backyard | ✓ | |

| Energy Efficiency | ✓ |

7. Stay Flexible and Realistic

While having a clear list of priorities is crucial, remain adaptable:

- Recognize that the perfect home may not exist, and compromises may be necessary.

- Focus on homes that meet at least 80-90% of your must-haves.

- Understand that certain features, such as renovations or landscaping, can be added later.

8. Revisit and Refine

Reevaluate your priorities periodically as you begin your search:

- After attending a few viewings, you may notice shifts in your preferences.

- Update your list based on what you learn about the market or your changing needs.

By carefully defining your priorities through these steps, you’ll lay a solid foundation for your home-buying journey, ensuring your search is focused, efficient, and aligned with your personal goals.

Step 2: Determine Your Budget

Establishing a clear budget is one of the most important steps in the home-buying process. It ensures you can afford your new home without financial strain and helps you focus your search on properties within your means. Here’s a comprehensive, step-by-step guide to help you calculate your maximum budget:

1. Assess Your Financial Resources

Start by taking stock of your current financial situation. This involves reviewing your income, savings, and any additional resources available for your home purchase.

- Calculate Your Savings:

- Review your bank accounts and investment portfolios to determine how much you can allocate for a down payment and closing costs.

- Remember to set aside an emergency fund for unexpected expenses after moving into your new home.

- Include Expected Financial Contributions:

- If family or friends are contributing to the purchase, include these funds in your total resources.

- Check for government grants or programs for first-time buyers in your region.

- Document Your Total Savings: Example:

| Source | Amount (in your currency) |

| Personal Savings | 50,000 |

| Family Contributions | 10,000 |

| Buyer Assistance Program | 5,000 |

| Total Available | 65,000 |

2. Understand Loan Options

Since most homebuyers rely on financing, understanding your loan options is critical to determining your maximum budget.

- Research Loan Types:

- Fixed-rate mortgages: Interest rate remains constant over the loan term.

- Variable-rate mortgages: Interest rates can fluctuate over time.

- Government-backed loans: These may offer lower interest rates or down payment requirements.

- Speak with a Mortgage Lender or Broker:

- Pre-qualify for a loan to understand how much you might be eligible to borrow.

- Ask for information on interest rates, repayment terms, and monthly installments.

- Calculate Your Potential Loan Amount: Use online mortgage calculators or consult with a lender to estimate the amount you can borrow based on your income, credit score, and debt-to-income ratio.

3. Factor in Additional Costs

Buying a home involves more than just the purchase price. Ensure you account for these costs in your budget:

- Down Payment:

- Typically ranges from 5-20% of the purchase price. For example, a home costing $300,000 may require a down payment of $15,000-$60,000.

- Closing Costs:

- These include legal fees, inspection fees, taxes, and insurance, often amounting to 2-5% of the home’s price.

- Ongoing Costs:

- Property taxes, homeowner’s insurance, and maintenance costs should be considered for long-term budgeting.

- Moving Costs:

- Include expenses for movers, packing supplies, and utility setup in your new home.

4. Calculate Your Maximum Budget

Combine all resources and anticipated loan amounts to determine your purchasing limit.

- Estimate Total Buying Power:

- Add your savings, contributions, and potential loan amount.

- Example:

| Source | Amount (in your currency) |

| Savings & Contributions | 65,000 |

| Loan Pre-Qualification | 200,000 |

| Total Budget | 265,000 |

- Set a Comfortable Range:

- While your maximum budget is essential, consider shopping below it to allow room for unexpected costs or upgrades.

- Review Affordability:

- A common rule is to allocate no more than 28-30% of your gross monthly income to housing costs, including mortgage, taxes, and insurance.

5. Plan for Financial Security

To protect yourself from financial strain, adopt strategies to ensure stability:

- Maintain an Emergency Fund:

- Retain at least 3-6 months of living expenses after buying the home.

- Anticipate Future Expenses:

- Consider upcoming life changes such as starting a family, career transitions, or retirement.

- Avoid Overextending Yourself:

- Stay within your budget even if you’re tempted by a higher-priced home.

6. Document Your Budget

Record your findings and share them with any stakeholders involved in the purchase. Use clear documentation to guide your decisions.

Example Budget Overview:

| Item | Amount (in your currency) |

| Savings | 65,000 |

| Loan Amount | 200,000 |

| Closing Costs (5%) | -15,000 |

| Down Payment (20%) | -60,000 |

| Emergency Fund Reserve | -10,000 |

| Available for Purchase | 180,000 |

7. Seek Professional Advice

Consult with professionals to refine your budget:

- Mortgage brokers: Help identify the best loan terms.

- Financial advisors: Provide long-term financial planning advice.

- Realtors: Help you identify properties within your price range.

By following these detailed steps, you’ll have a clear understanding of your financial capabilities and be prepared to make informed decisions during your home-buying journey. Proper budgeting is not just about numbers; it’s about building confidence and ensuring long-term satisfaction in your new home.

Step 3: Research Financing Options

Understanding financing options is a crucial step in the home-buying process. With various types of mortgages available, choosing the one that best fits your financial situation can significantly impact your homeownership experience. This step-by-step guide walks you through the process of researching, comparing, and selecting the most suitable financing option.

1. Understand the Basics of Mortgages

Before diving into the details, familiarize yourself with how mortgages work.

- What is a Mortgage?

- A mortgage is a loan specifically designed to help you purchase property.

- It typically involves a down payment, a principal loan amount, and interest that you pay back over time.

- Components of a Mortgage:

- Principal: The original loan amount you borrow.

- Interest Rate: The cost of borrowing, expressed as a percentage of the loan.

- Loan Term: The duration over which the loan is repaid, usually 15, 20, or 30 years.

- Monthly Payments: Consist of principal repayment, interest, taxes, and insurance (often abbreviated as PITI).

- Key Terms to Know:

- Fixed-rate mortgage: The interest rate remains constant throughout the loan term.

- Adjustable-rate mortgage (ARM): The interest rate changes periodically after an initial fixed-rate period.

- Loan-to-value ratio (LTV): The percentage of the home’s price financed by the loan.

- Debt-to-income ratio (DTI): Your monthly debt obligations divided by your gross monthly income, expressed as a percentage.

2. Explore Types of Mortgages

Each mortgage type has unique features, advantages, and potential drawbacks. Explore these common options:

- Fixed-Rate Mortgages:

- Pros: Predictable monthly payments and protection against rising interest rates.

- Cons: Typically higher initial interest rates than ARMs.

- Best for: Buyers who plan to stay in their home long-term and prefer financial stability.

- Adjustable-Rate Mortgages (ARMs):

- Pros: Lower initial interest rates compared to fixed-rate mortgages.

- Cons: Payments may increase significantly after the fixed period ends.

- Best for: Buyers planning to sell or refinance before the adjustable rate begins.

- Government-Backed Loans:

- Examples:

- FHA Loans: Low down payments; ideal for first-time buyers.

- VA Loans: Exclusive to veterans; offers favorable terms with no down payment.

- USDA Loans: Designed for rural property buyers; offers low interest rates.

- FHA Loans: Low down payments; ideal for first-time buyers.

- Interest-Only Mortgages:

- Pros: Lower initial monthly payments as you pay only the interest for a specified period.

- Cons: Payments increase later when principal payments begin.

- Best for: Buyers with irregular or fluctuating income.

- Balloon Mortgages:

- Pros: Smaller monthly payments until a large payment (the “balloon”) is due at the end.

- Cons: Requires a large lump sum payment.

- Best for: Buyers planning to sell or refinance before the balloon payment.

3. Assess Your Financial Situation

Your financial profile will influence which financing options are available and suitable for you.

- Evaluate Your Credit Score:

- A higher credit score typically qualifies you for lower interest rates.

- Request your credit report and address any inaccuracies before applying for a mortgage.

- Determine Your Down Payment Capability:

- Conventional loans often require 20% down, but government-backed loans may allow for lower percentages.

- Consider the impact of a higher down payment on reducing your monthly payments and avoiding private mortgage insurance (PMI).

- Calculate Your Debt-to-Income Ratio (DTI):

- Most lenders prefer a DTI of 43% or lower.

- Use this ratio to assess your borrowing capacity.

4. Compare Offers from Multiple Lenders

Different lenders offer varying terms, so it’s important to shop around.

- Request Pre-Approvals:

- Obtain pre-approvals from several lenders to understand your borrowing potential.

- Pre-approvals provide estimated loan amounts, interest rates, and monthly payments.

- Review Interest Rates and Loan Terms:

- Compare fixed vs. adjustable rates and consider the total cost of borrowing over the loan term.

- Look beyond the interest rate—pay attention to fees, closing costs, and prepayment penalties.

- Ask About Fees and Hidden Costs:

- Inquire about origination fees, appraisal fees, and other closing costs.

- Clarify whether the lender offers discounts or incentives for certain loan types.

- Negotiate Terms:

- Use competing offers to negotiate better terms with your preferred lender.

5. Decide Which Option Suits You Best

Once you’ve compared options, narrow down your choices based on your long-term financial goals.

- Match the Loan to Your Needs:

- Consider how long you plan to stay in the home.

- For short-term stays, ARMs may be advantageous. For long-term stability, a fixed-rate mortgage is better.

- Factor in Future Plans:

- Think about career changes, family growth, or retirement, and how these may affect your ability to repay the loan.

- Choose a Loan You Can Comfortably Afford:

- Avoid stretching your budget. Choose a loan that leaves room for savings and unforeseen expenses.

6. Consult Experts

Before making a final decision, seek advice from professionals who can guide you through the complexities of mortgage selection.

- Mortgage Brokers:

- Can provide a variety of loan options and negotiate with lenders on your behalf.

- Financial Advisors:

- Help you assess long-term affordability and overall financial impact.

- Real Estate Agents:

- Offer insights on local market trends and recommend trusted lenders.

7. Finalize Your Financing Choice

After thorough research and consultation, finalize the financing option that aligns with your priorities. Make sure all terms are clearly documented in the loan agreement.

By carefully researching and selecting the right financing option, you’ll lay a strong foundation for a successful home purchase and long-term financial security.

Step 4: Set Realistic Expectations

Setting realistic expectations is crucial for a smooth home-buying experience. By understanding what’s achievable within your budget and aligning it with current market conditions, you can make informed decisions, avoid disappointment, and stay within financial boundaries. This guide will walk you through the process step by step.

1. Understand the Concept of Realistic Expectations

Before diving into specifics, it’s important to define what “realistic expectations” means in the context of home buying.

- Balance Needs and Wants:

- Realistic expectations involve finding a balance between your priorities (must-haves) and preferences (nice-to-haves).

- Remember that compromise is often necessary, especially in competitive markets.

- Be Aware of Market Constraints:

- The availability of homes that fit your criteria may be limited by your budget and local real estate conditions.

- Recognizing market constraints helps prevent frustration and wasted time.

- Adapt to Your Financial Situation:

- Your budget, financing options, and future financial goals play a significant role in shaping what is feasible.

2. Research Current Market Conditions

The real estate market is dynamic, and conditions can vary significantly based on location, season, and economic trends.

- Understand Local Market Trends:

- Research recent property sales in your desired area to get an idea of current price ranges.

- Use online platforms, real estate listings, and market reports to gather data.

- Evaluate the Market Type:

- Buyer’s Market: When supply exceeds demand, buyers have more negotiating power, and prices are generally lower.

- Seller’s Market: When demand exceeds supply, competition drives prices up, and offers may need to exceed the asking price.

- Monitor Interest Rates and Loan Terms:

- Rising interest rates may reduce your borrowing power, while lower rates can increase affordability.

- Keep track of economic news and consult lenders for updates.

- Factor in Seasonal Trends:

- Spring and summer often see more properties listed but also more competition.

- Winter months may offer better deals, although inventory might be limited.

3. Align Your Expectations with Your Budget

Your budget sets the framework for what’s realistic. Here’s how to ensure your expectations are in line with your financial capabilities:

- Review Your Maximum Budget:

- Confirm the maximum amount you’re willing and able to spend, considering down payments, monthly mortgage payments, and additional costs.

- Break Down Costs Beyond the Purchase Price:

- Closing Costs: Include legal fees, inspection fees, and taxes.

- Ongoing Costs: Account for maintenance, insurance, and property taxes.

- Potential Renovation Costs: Budget for repairs or upgrades needed to make the home move-in ready.

- Match Your Budget to Local Property Prices:

- Compare your budget to the average property prices in your preferred areas.

- Consider expanding your search radius if prices in your ideal location exceed your budget.

- Focus on Long-Term Affordability:

- Choose a home that not only meets your immediate needs but is also affordable over the long term.

4. Narrow Down Your Expectations

Now that you have a clear understanding of market conditions and budget constraints, refine your expectations.

- Revisit Your Priority List:

- Separate your must-haves from your nice-to-haves once more.

- Adjust your list based on what the market and your budget allow.

- Example: If homes with large gardens are out of your budget, consider properties with smaller outdoor spaces or communal gardens.

- Be Open to Alternatives:

- Explore nearby neighborhoods or suburbs if your preferred area is too expensive.

- Consider different property types, such as condos or townhomes, if single-family homes exceed your budget.

- Set Realistic Size and Feature Expectations:

- Recognize that features like extra bedrooms, luxury finishes, or prime locations often come at a premium.

- Decide what compromises you’re willing to make, such as opting for a smaller home or one that requires minor renovations.

- Prepare for Trade-Offs:

5. Seek Professional Guidance

Real estate professionals can help you align your expectations with reality.

- Consult a Real Estate Agent:

- An experienced agent can provide insights into what’s realistic within your budget and chosen market.

- Agents can also recommend neighborhoods and properties that fit your criteria.

- Talk to Financial Advisors:

- Financial advisors can help you understand the long-term implications of your home purchase.

- They can also suggest ways to increase your affordability through savings or loan adjustments.

- Attend Open Houses:

- Visiting properties helps you see what’s available at different price points and refine your preferences accordingly.

- Take notes on features, layouts, and prices to build a clearer picture of what’s realistic.

6. Set Clear Expectations for the Buying Process

Understanding what to expect during the home-buying process can help manage your overall outlook.

- Timeframe:

- Be prepared for a lengthy process, especially in competitive markets.

- Setting a realistic timeline can reduce stress and keep you focused.

- Negotiation:

- Understand that negotiations may not always lead to significant price reductions, especially in a seller’s market.

- Focus on negotiating for favorable terms, such as including appliances or covering closing costs.

- Flexibility:

- Maintain flexibility with your expectations. If a home meets 80-90% of your criteria, it might be worth considering.

- Be open to reevaluating your priorities if necessary.

By setting realistic expectations, you position yourself for success in the home-buying process. This approach ensures that your financial goals align with market conditions and that you remain adaptable throughout the journey. Making informed decisions will help you find a home that meets your needs and brings long-term satisfaction.

We’re also giving these extra bonuses

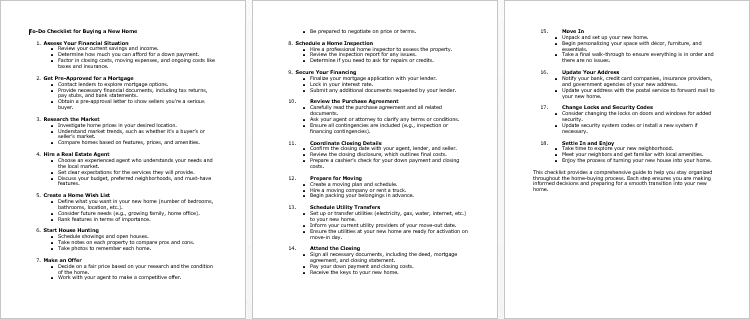

Buying a New Home – Checklist

Buying a New Home – FAQs

Buying a New Home – Salespage Content

Package Details:

Word Count: 24 850 Words

Number of Pages: 100

Buying a New Home – Bonus Content

Checklist

Word Count: 667 words

FAQs

Word Count: 1077 words

Salespage Content

Word Count: 850 words

Total Word Count: 27 444 Words

Your PLR License Terms

PERMISSIONS: What Can You Do With These Materials?

Sell the content basically as it is (with some minor tweaks to make it “yours”).

If you are going to claim copyright to anything created with this content, then you must substantially change at 75% of the content to distinguish yourself from other licensees.

Break up the content into small portions to sell as individual reports for $10-$20 each.

Bundle the content with other existing content to create larger products for $47-$97 each.

Setup your own membership site with the content and generate monthly residual payments!

Take the content and convert it into a multiple-week “eclass” that you charge $297-$497 to access!

Use the content to create a “physical” product that you sell for premium prices!

Convert it to audios, videos, membership site content and more.

Excerpt and / or edit portions of the content to give away for free as blog posts, reports, etc. to use as lead magnets, incentives and more!

Create your own original product from it, set it up at a site and “flip” the site for megabucks!

RESTRICTIONS: What Can’t You Do With These Materials?

To protect the value of these products, you may not pass on the rights to your customers. This means that your customers may not have PLR rights or reprint / resell rights passed on to them.

You may not pass on any kind of licensing (PLR, reprint / resell, etc.) to ANY offer created from ANY PORTION OF this content that would allow additional people to sell or give away any portion of the content contained in this package.

You may not offer 100% commission to affiliates selling your version / copy of this product. The maximum affiliate commission you may pay out for offers created that include parts of this content is 75%.

You are not permitted to give the complete materials away in their current state for free – they must be sold. They must be excerpted and / or edited to be given away, unless otherwise noted. Example: You ARE permitted to excerpt portions of content for blog posts, lead magnets, etc.

You may not add this content to any part of an existing customer order that would not require them to make an additional purchase. (IE You cannot add it to a package, membership site, etc. that customers have ALREADY paid for.)

Deprecated: Function post_permalink is deprecated since version 4.4.0! Use get_permalink() instead. in /home/buyqualityplr/public_html/wp-includes/functions.php on line 6121

Share Now!

Latest Products

Free Sales Funnel Builder

Related Products

Popular & Trending

Featured Products